Dear friends,

We hope this letter finds you well. In this letter, we provide commentary on U.S. stocks, the “magnificent seven” and geopolitical headlines including tariff threats.

Given the threat of tariffs that has dominated the news cycle, many of you might ask, “What impact will potential U.S. tariffs on Canadian, Mexican and Chinese goods have on our investments?” To us, President Trump’s rhetoric on trade and tariffs sounds counterproductive and misguided. Tariffs are harmful to all parties. It is important to note that countries do not engage in trade with each other — only businesses and individuals do. When individuals or businesses engage in trade, both parties — the buyer and the seller — are made better off. Trade is “win-win”. The great economist Thomas Sowell has this to say on U.S. President Trump’s tariff threats: “You do not make America great again by raising the price to Americans, which is what a tariff does.” In an interview with Reason magazine, Sowell had this to say when asked about his thoughts on the Trump trade war:

“Oh my gosh, an utter disaster. I happen to believe that the Smoot-Hawley tariffs had more to do with setting off the Great Depression of the 1930s than the stock market crash. Unemployment never reached double digits in any of the 12 months that followed the crash of October 1929, but it hit double digits within six months of passage of Smoot-Hawley, and stayed there for a decade[1]”.

Consider oil and gas, Canada’s largest export to the U.S. It is a commodity that, despite the claims of the 47th President, the U.S. does, in fact, need and want. Eric Nuttall, a partner and senior portfolio manager at NinePoint Partners, said in a recent interview with BNN Bloomberg that he is “optimistic” that the pain of tariffs between Canada and the U.S. would be “so profound” for both nations that it would make for a short dispute[2]. He said that it is “very clear” the U.S. needs Canadian oil, and that “they have no alternative.” He explains that “Canada is a critical component to the United States’ energy independence. We account for just over 60 per cent of their net oil imports, as each day they produce 13.3 million barrels of oil and consume 20.5 million. Their production is a light oil, and is not well suited for the majority of the U.S. refinery complex which was built to process Canadian heavy oil, never with the thought of not having access to the U.S.’s safest, most reliable and cheapest source of oil. How will refineries around the Chicago area that import three million barrels of oil per day to be turned into higher-value gasoline and diesel possibly replace our pipeline-connected oil at scale? With barges and trucks?[3]” Nuttall predicts that U.S. gas prices could rise around 15 to 20 cents per gallon, based on the proposed 10% tariff.

Trump’s rationale for tariffs is based on the long-standing theory that the U.S. is at a disadvantage in world trade, owing to the strength of the U.S. dollar, which in turn is the result of its position as the world’s reserve currency. In a recent FP article, Father Raymond J. DeSouza explained that “The strong dollar makes it relatively cheaper for Americans to buy foreign goods — imports increase. American exports become more expensive abroad. This can lead to a trade deficit, which means a country imports more than it exports.[4]”

Economist Stephen Miran, Trump’s pick to lead his Council of Economic Advisors, has Trump’s ear with respect to tariffs. Miran’s theory about tariffs is arcane and it rests on anticipated currency movements to blunt the impact of higher prices for U.S. consumers (i.e. inflation). De Souza breaks it down as follows:

“Follow carefully: The U.S. trade deficit is caused by an overvalued U.S. dollar; tariffs make imports more costly, reducing the trade deficit; inflation rises, as do American interest rates; capital flows into the U.S.; the U.S. dollar rises, making imports cheaper; the trade deficit grows.” It is a bet that the benefits will outweigh the negatives. As DeSouza explains: “Showing a remarkable confidence in economic policy-making, Miran argues that the relative quantities of these shifts can be carefully managed such that the benefits are greater than the costs.” Perhaps, but the Trump / Miran tariff strategy involves a daisy chain of events with intractable second-order effects, in our view. Much can go wrong. Sowell had this to say about Trump’s tariffs in 2018: “When you set off a trade war, like any other war, you have no idea how that is going to end. You’re going to be blindsided by all kinds of consequences[5].”

Further, economies are profoundly complex, and do not lend themselves well to such top-down tinkering or planning. The Nobel-winning economist Frederick Hayek agrees. Writing in the Financial Post, Matthew Lau summarized Hayek’s Nobel Prize acceptance speech as follows: “When economists or other experts wrongly believe they have the data and knowledge to precisely fine-tune the economy through top-down initiatives, disasters ensue[6].”

The Trump / Miran plan may have unintended and adverse consequences that are politically unpalatable. After all, didn’t Mr. Trump campaign on the promise to halt inflation and make life more affordable? Writing in The Free Press, under headline “Is This What America Voted For?”, Ruy Texeira warns that U.S. voters care about the cost of living, which appears to be at odds with a plan to impose tariffs: “Warning signs are flashing on a clear voter priority: the economy. In the Washington Post poll, 76 percent of respondents rate current gas or energy prices either “not so good” or “poor,” 73 percent said the same of the incomes of average Americans, and 92 percent said it about food prices. In [a] CNN poll, only 27 percent think Trump has been “about right” on trying to reduce the price of everyday goods[7]”.

Politico financial writer Sam Sutton summed it up as follows: “A central question of Trump 2.0 will be the extent to which both financial markets and the political class will be able to stomach the tumult that would accompany any attempt to reshape global trade, particularly if the economic outcome proves to be more painful than many of Trump’s advisers contend.[8]”

A related question is, “Should investors reposition their investments because of today’s geopolitical uncertainty?” We generally do not try to predict the “macro” (i.e. the future path of the economy, interest rates, currency movements, tariff impacts, etc.) and we do not recommend that investors tinker with their investments based on a macro view. There are many unknowns in the brewing trade war. Are Trump’s threats sincere or are they being used as leverage to alter trade agreements or to gain some other policy objective (e.g. border security)? Will U.S. tariffs be a short-term phenomenon? We suspect, as do most people, that Trump’s tariff plan will be damaging – economically for all parties, and politically for the U.S. President. Our view is that U.S. tariffs will fail as an experiment and may be short-lived, as the economic pain will be costly to the President in terms of political currency. We view U.S. tariffs as just the latest in an ever-present list of geopolitical worries – a “wall of worry” that confronts markets and investors. We do not mean to downplay the potential impact of tariffs. Our guess is that it in the worse case scenario – a long-term trade war featuring escalation and retaliation, the impact to the Canadian economy will be significant. But we argue that a drawn-out trade war is in no one’s interest, so it is not likely.

It is a natural reaction when confronted with negative headlines such as today’s tariffs, to do something – to take action. It is counterintuitive to do nothing, because burying your head in the sand is a poor strategy in most other endeavours. But doing nothing is precisely what we recommend. In investing, less is more. As John Bogle often quipped to Vanguard investors, “Don’t just do something. Stand there.” Why not sell your stocks and wait out the looming threat? The problem is that we do not have better insight than the mass of investors that make up the market. They’ve all watched the news. Furthermore, such a strategy requires that you are right twice – selling in anticipation of a decline and buying back in before a rebound. Again, you must have better insight than the masses. This is not likely.

One investment strategy, referred to as “macro” investing, seeks to try and predict the future path of things like the stock market, inflation, the economy, etc., and position investments based on this “top-down” forecast. The macro investor may, for example, try to buy and sell stocks based on a forecast of tariff impacts. This sounds logical. The problem is that economic forecasts have a dismal predictive record. Even the Federal Reserve has not been able to predict macro events, as evidenced by the woeful track record of its “forward guidance”. Howard Marks explains:

“Humility may even be seeping into one of the world’s biggest producers of economic forecasts, the U.S. Federal Reserve, home of more than 400 Ph.D. economists. Here’s what economist Gary Shilling wrote in Bloomberg Opinion on August 22:

The Federal Reserve’s forward guidance program has been a disaster, so much so that it has strained the central bank’s credibility. Chair Jerome Powell seems to agree that providing estimates of where the Fed sees interest rates, economic growth and inflation at different points in the future should be junked. . . .”

In 2022, Marks also summarizes the dreadful track record of hedge funds that employ a “macro” strategy[9]:

“Hedge Fund Research (HFR) publishes broad hedge fund performance indices as well as a number of sub-indices. Below is the long-term performance of a broad hedge fund index, a macro fund sub-index, and the Standard & Poor’s 500 Index”.

Marks asks, rhetorically, “Where are the people who’ve gotten famous (and rich) by profiting from macro views?[10].” That the macro investors continue with their strategy is a triumph of hope over experience.

Rather than make guesses about the macro, our strategy is characterized as “bottom up.” We spend most of our time researching and thinking about the “micro” (companies, industries, and securities). We like to buy companies that are likely to endure adversity and to hold them through thick and thin. We leave the guesswork on macro events to others. In our last correspondence, we talked about “quality” investing. The impact of tariffs is an example of the near-infinite factors that can influence markets. There are unknowns and there are also “unknown unknowns” (i.e. risks that were not even considered). Due to the multitude of risks that come with investing in stocks, we advocate for buying quality. We like to buy what is hard to kill, and this durability is the primary filter that we use in picking stocks. To the investor in wide-moat and durable stocks, tariffs may impact near-term values, but the long-term prospects are more likely to remain intact, relative to lesser-advantaged peers. The astute and intrepid investor can also look upon volatility from tariffs as an opportunity to find bargains. We will be monitoring our buy list.

Turning to the topic of the stock market, many of you will know that the S&P 500 posted back-to-back calendar year returns more than 20% in 2023 and 2024. Canadian investors in U.S. stocks further benefited from a weak Canadian dollar. Some, expecting the pendulum to swing the other way, understandably ask, “Aren’t we do for a correction?

The answer to that question is probably but not necessarily. It is probable because stocks typically experience a 5-10% correction every few years. Over a decade or so, it is not uncommon to see a drop of 15-25%. It is tempting to try and sidestep corrections, but alas their timing is devilishly unpredictable – it is, on average, a loser’s game. The same is true for individual stocks. It is natural for investors to feel a need to “protect” large gains, or trim their holdings after a lengthy advance. After all, the investment industry often counsels investors to “rebalance” their portfolios. An old market adage is that “you never go broke taking a profit.” This is true, but importantly, you never get very rich either.

In our experience, selling your stocks based on macro worries more often than not detracts value. Compounding requires patience and such “tinkering” disrupts the process. Stocks don’t rise in a straight line. In fact, stocks often follow a step-like pattern, with sharp increases followed by periods of stagnation or even crisis or “correction”, and then sharp rises again. The problem is that sharp increases often go on much longer than anticipated, and the end of corrective phases (such a pleasant-sounding euphemism) is never obvious until its too late. More often than not, the investor who seeks to outsmart the market is humbled and they later regret missing out on long-term gains. Allow us to cherry-pick an example. There were many occasions over the past 25 years that shares of Amazon looked expensive (and the broad market, too) but it was a mistake to tinker with this long-term compounder. Over the past 20 years through Dec. 30, 2024, Amazon shares have generated a total return of 9,736% compared to a 387% total return for the S&P 500 during that stretch. Those gains translate to a 25.8% compound annual growth rate for Amazon compared to an 8.2% CAGR for the S&P 500 in that time[11]. Over that 20-year period, there were many significant drawdowns, and there was a wall of worry to climb about not only Amazon, but the economy, geopolitics, etc. Possessing the equanimity to hang on to investments is truly a superpower. The great Peter Lynch said it best: “Far more money has been lost by investors trying to anticipate corrections, than lost in the corrections themselves.”

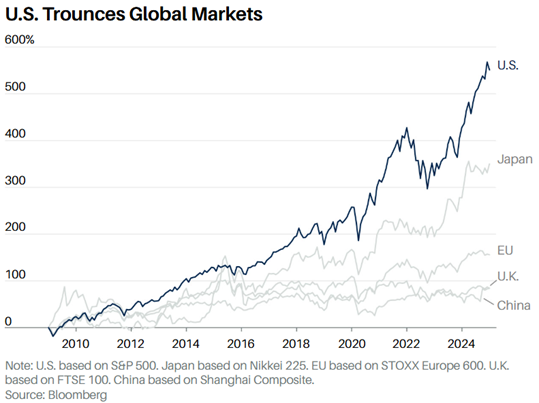

You may also be aware that the U.S. stock market has significantly outperformed markets elsewhere in the world (see chart below), leading many to wonder whether it can last or will returns “mean-revert.” A big part of this outperformance is due to the strong performance of U.S. technology stocks, which make up north of 40% weighting of the S&P500.

Here is a statistic that may surprise you: “Since the late 1980s, U.S. stocks have increased by 25 times, while European stocks have risen by less than six[12].” Some may take this outperformance as an indicator that U.S. stocks are expensive and that some combination of lower U.S. returns and higher, say EU stock returns are inevitable. Our view is this: don’t bet on it. Furthermore, we believe that the conditions that led to this striking outperformance remain in place and are likely to persist. So does Todd Ahlsten, chief investment officer at Parnassus Investments. In a recent Barron’s discussion, he commented that the S&P 500 is “awesome”. He explains that, “Think about the innovation in cloud computing, semiconductors, life sciences, industrial automation, transportation, electrification. This index is a collection of advantaged assets that continue to get more advantaged. TAMs [total addressable markets] are increasing, as are profit margins.” Like us, Ahlsten sees U.S. markets as “advantaged.” The U.S. is a petri dish of innovation, a bastion of free enterprise with and entrepreneurial culture. It also boasts the most liquid markets and the most vibrant financial system – one that aids capital formation. The U.S. attracts capital from all over the world because it is acknowledged as the best place to invest. To use an analogy, we understand that 98% of tornadoes happen in the Midwest U.S., as this is the only place where all the conditions necessary to produce a tornado exists in the world. Other areas have some of the requisite conditions, but that is not enough – they rarely, if ever, experience tornadoes. Like the phenomenon of tornadoes, the U.S. market has all the key conditions that have led to outperformance, and we do not see that changing anytime soon. In his most recent letter to Berkshire Hathaway investors, Warren Buffett had this to say about the exceptionalism of U.S. markets: “as Charlie and I have always acknowledged, Berkshire would not have achieved its results in any locale except America.[13]”

Another brick in today’s wall of worry is the concentration of the so-called “magnificent seven” (Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta and Tesla), in terms of weighting in the S&P500 index. These seven companies together constitute a 32% weighting. As noted by Howard Marks in a recent memo to clients, past “bubbles”, including the “TMT” (technology, media, telecom) bubble in the late 1990’s were characterized by similar levels of concentration. Naturally, some investors look upon the concentration of the “mag seven” as a possible indicator of a bubble á la 1999. But an important caveat: Unlike previous eras, in which a popular group of stocks reached extreme valuations, we do not witness that in today’s “mag seven.” Marks cedes this point: “today’s leaders don’t trade at the p/e ratios investors applied to the Nifty Fifty. Perhaps the sexiest of the seven is Nvidia, the leading designer of chips for artificial intelligence. It’s current multiple of future earnings is in the low 30s, depending on which earnings estimate you believe”.

Importantly, the magnificent seven do not sport extreme valuations. Sure, the share prices have gone up a lot over the past several years but so has the mountain of cash generated by these companies. Apple has returned just under $1 trillion to investors since 2013 (i.e. in the form of dividends and share repurchases)[14]. In 2024 Alphabet returned about $70 billion to shareholder in the form of buybacks and dividends[15]. In 2018 they returned a total of $8 billion to shareholders[16]. Investments are worth what they produce, whether it is a cow, a farm, or shares of a company, and boy, have the magnificent seven been producing.

Put simply, the magnificent seven may not prove to be overvalued considering their highly attractive economics, long runway for growth and competitive edges.

Further, the magnificent seven are not anything like the companies that were heavily weighted in the S&P in past eras seen today as “bubbles.” Here is Marks to explain:

“Today’s S&P-leading companies are, in many ways, much better than the best companies of the past. They enjoy massive technological advantages. They have vast scale, dominant market shares, and thus above average profit margins. And since their products are based on ideas more than metal, the marginal cost of producing an additional unit is low, meaning their marginal profitability is unusually high.”

The magnificent seven are much different than the market darlings that led the TMT bubble. In that era, newer companies with little-to-no earnings, and no established competitive advantages were bid up to extraordinary valuations. Many were “pie in the sky” type companies – some were mere lottery tickets. In contrast, the magnificent seven gush cash, have a long runway for growth (which is abetted by the exciting long-term prospects of AI) and, generally have moats that are getting deeper and wider. For these reasons, the concentration of the mag seven in the S&P 500 may not be as worrisome as some might predict.

As always, we are here to provide you with reassurance and to help if you have questions.

Best wishes to you and your family from your APEX team: Shawn, Mike, Denise N., Lisa, Marta, Denise E., John, Will and Jeannot.

Disclaimer:

This publication is for informational purposes only and has been prepared from public sources which are meant to be reliable. None of the information in this should be construed as investment advice. Speak to your Investment Advisor to learn if this product is right for you. Apex Investment Management is a tradename of Designed Securities Ltd. DSL is regulated by the Canadian Investment Regulatory Organization and a Member of the Canadian Investor Protection Fund Michael Begg and Shawn Malcolm are registered to advise in securities and/or mutual funds to clients residing in Ontario and B.C. The views expressed are those of the author and not necessarily those of DSL.

[1] Perry, Mark. “Thomas Sowell on Trump’s Trade War and Trump’s View on Trade Surpluses.” American Enterprise Institute – AEI, 25 May 2022, www.aei.org/carpe-diem/thomas-sowell-on-trumps-trade-war-and-trumps-view-on-trade-surpluses.

[2] Johnson, Daniel. “Eric Nuttall Says the U.S. Has ‘No Alternative’ to Replace Canadian Oil.” BNN Bloomberg, 3 Feb. 2025, www.bnnbloomberg.ca/investing/commodities/2025/02/03/eric-nuttall-says-the-us-has-no-alternative-to-replace-canadian-oil.

[3] “Eric Nuttall: Now Is the Time to Unleash Canada’s Enormous Resource Potential.” Financial Post, 4 Feb. 2025, financialpost.com/commodities/energy/oil-gas/now-time-unleash-canada-enormous-resource-potential.

[4] “Raymond J. De Souza: Trump Wants Tariffs With No Tradeoffs. It Won’t Happen.” National Post, 12 Feb. 2025, nationalpost.com/opinion/trump-wants-tariffs-with-no-tradeoffs-it-wont-happen.

[5] Perry, Mark. “Thomas Sowell on Trump’s Trade War and Trump’s View on Trade Surpluses.” American Enterprise Institute – AEI, 25 May 2022, www.aei.org/carpe-diem/thomas-sowell-on-trumps-trade-war-and-trumps-view-on-trade-surpluses.

[6] “Matthew Lau: Fifty Years on, a Nobel Lecture Everyone Should Read on Why Central Planning Always Fails.” Financial Post, 16 Oct. 2024, financialpost.com/opinion/nobel-lecture-why-central-planning-always-fails.

[7] Teixeira, Ruy. “Is This What America Voted For?” The Free Press, 27 Feb. 2025, www.thefp.com/p/is-this-what-america-voted-for?utm_source=substack&utm_medium=email.

[8] “Why Stephen Miran thinks tariffs can work.” Politico.com, 6 Jan. 2025, www.politico.com/newsletters/morning-money/2025/01/06/why-stephen-miran-thinks-tariffs-can-work-00196532.

[9] “The Illusion of Knowledge.” Oaktree Capital , 8 Sept. 2022, www.oaktreecapital.com/insights/memo/the-illusion-of-knowledge.

[10] Ibid.

[11] How Much Would $10,000 Invested in Amazon Stock 20 Years Ago Be Worth Today?, US News, December 31, 2024, https://money.usnews.com/investing/articles/how-much-would-invested-in-amazon-stock-worth-today

[12] Masoni, Danilo. “European Stocks Step Out From U.S. Shadow in 2025, but for How Long.” The Globe and Mail, 6 Feb. 2025, www.theglobeandmail.com/investing/article-european-stocks-step-out-from-us-shadow-in-2025-but-for-how-long/#:~:text=Since%20the%20late%201980s%2C%20U.S.,Wall%20Street’s%20long%2Dterm%20dominance.

[13] BERKSHIRE HATHAWAY INC. www.berkshirehathaway.com/letters/2024ltr.pdf.

[14] Ward, Sandy. “What Apple’s Cash ‘Problem’ Means for Its Stock Investors.” Morningstar, Inc., 10 May 2023, www.morningstar.com/markets/what-apples-cash-problem-means-its-stock-investors.

[15] “2024 Q4 Earnings Call – Alphabet Investor Relations.” Alphabet Investor Relations, abc.xyz/2024-q4-earnings-call/#:~:text=In%20Q4%2C%20we%20returned%20value,billion%20to%20shareholders%20in%202024.

[16] Google 10-K, 2018. https://www.sec.gov/Archives/edgar/data/1652044/000165204419000004/goog10-kq42018.htm the best approach to balance investors’ desire for growth and dividend income with the risk of investing in stocks.